Grain traders wait on US–Iran peace deal negotiations

Our benchmark spot prices (Midlands & Wales)

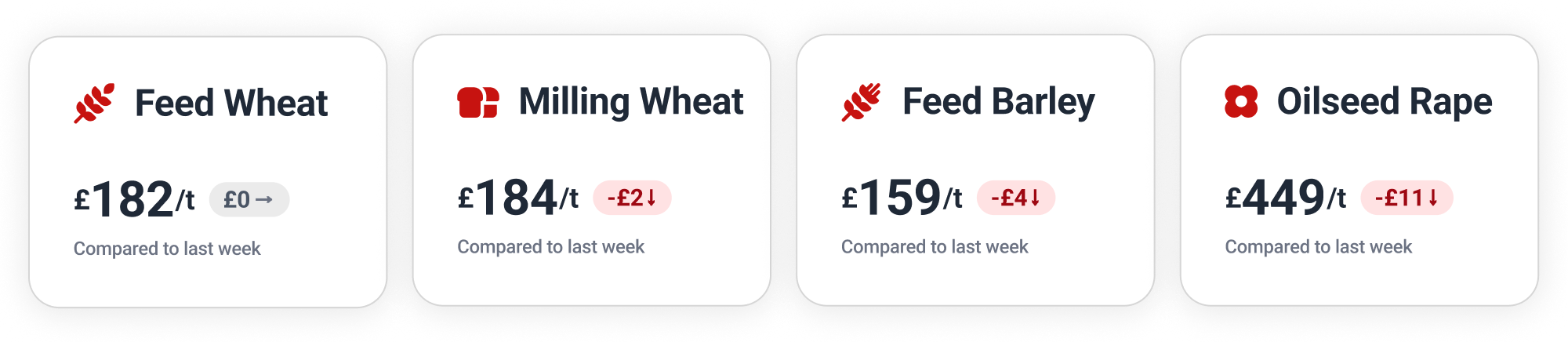

Feed Wheat

The prospect of a US–Iran peace deal has hung over the grain markets in the past few days, as traders weigh whether this is another false dawn.

Meanwhile in Ukraine, wheat exports accelerated significantly in April to 1.3 million tonnes, although diplomatic friction continues over Egypt’s acceptance of stolen grain. Ukraine has now demanded Israel conduct laboratory analyses on 16.5 thousand tonnes of wheat aboard the Russian ship Abinsk.

India, the world’s second-largest wheat producer, has exported wheat for the first time since 2022, capitalising on high domestic supply and rising global prices to ship 22,000 tonnes to the UAE.

London feed wheat (May 2026) has eased back since hitting £190.20 last Wednesday. Following the long weekend, the “old crop” contract dropped to £186.80 on Tuesday and £186.30 by Wednesday’s close. A lack of further momentum saw the contract finish Thursday at £188.00.

Farmers on Hectare Trading have been forward-selling 2026 feed wheat in Mid Wales, North East Scotland and East Anglia, and 2027 crop in Northumberland & Scottish Borders.

For full spot and futures price analysis, visit our enhanced Insights on Hectare Trading.

Milling Wheat

In Europe, much-needed rainfall has eased crop concerns, prompting the EU Commission to raise its soft wheat production estimate to 127.3 million tonnes.

UK winter wheat conditions have declined following a dry April, with 74% rated good or excellent (down from 82% in March). Putting this news into perspective, only 31% of the US winter wheat crop is rated in good or excellent condition, with severe production risks for the hard red winter wheat crop in Kansas and Oklahoma.

After retreating to €213.50 (£184.12) last Thursday ahead of the French market holiday, Paris milling wheat (September 2026) has declined steadily this week. The contract dropped to €207.50 (£179.22) by Wednesday’s close, and to €206.50 (£178.64) on Thursday.

Feed Barley

According to AHDB data, the condition of UK winter barley has declined. Currently, 70% of winter barley is rated good or excellent, a drop from 85% in late March but higher than the April scores seen in 2024 and 2025.

With UK spring barley planting intentions down 15% year-on-year, it was no surprise to see the US Foreign Agricultural Service project a fall in UK barley production for 2026/27 to 6.2 million tonnes, from 6.5 million tonnes last year.

Oilseeds

US soybean markets have been supported by hopes for increased trade following the Trump–Xi summit. Furthermore, the US Environmental Protection Agency’s ambitious new biofuel blending targets have forced producers to ramp up output, sending US soybean oil prices to their highest levels since spring 2022.

The EU has lifted its 2026/27 rapeseed production estimate to 20.8 million tonnes, while Canadian canola stocks have jumped 27.4% year-on-year to 10.0 million tonnes due to record production in 2025.

Having risen €90 from €438.00 (£382.20) at the end of last year to €528.00 (£455.97) on Monday, Paris rapeseed (August 2026) has weakened slightly over the past few days. With Brent crude retreating from its April highs, rapeseed has lost some impetus, the August 2026 contract closing Thursday at €509.75 (£440.99).

Wanted Crop

🌾 Feed wheat is wanted for collection in Yorkshire and the Humber for movement this month, with a guide price of £186–190/t ex-farm.

🌾 Feed wheat required for collection in the East Midlands. May movement with a guide price of £180–185/t ex-farm.

🌾 Feed wheat is wanted for collection in East Anglia. Movement in May or June, with a guide price of £175–180/t ex-farm.

🌾 Feed barley required for collection in Yorkshire and the Humber for movement this month, with a guide price of £166–170/t ex-farm.

🌾 Feed wheat is wanted for collection in Yorkshire and the Humber. Movement in May or June, with a guide price of £180–185/t ex-farm.

🌾 Feed wheat required for collection in Wales, the West Midlands and the North West. May or June movement, with a guide price of £185–193/t ex-farm.

This article is for general information only and does not constitute advice. While we make every effort to ensure the accuracy of the content at the time of publication, Hectare Trading makes no guarantee regarding the data provided.