US–Iran ceasefire has renewed uncertainty

Our benchmark spot prices (East Midlands)

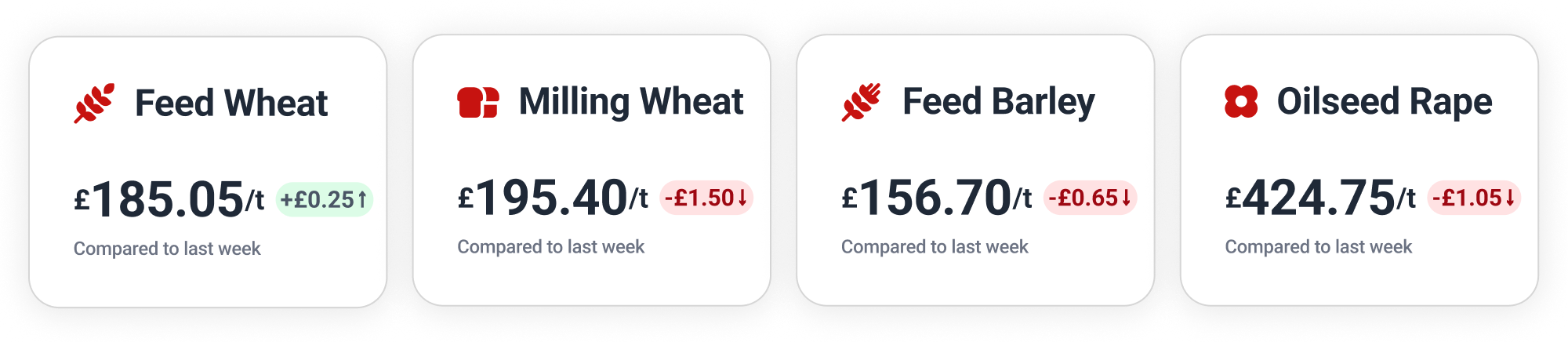

Feed Wheat

The collapse of the US–Iran ceasefire has renewed uncertainty for farmers, sparking fears of vessel disruptions in the Strait of Hormuz and sending crude oil prices higher.

While the early harvest in Ukraine and Romania has started with high yields, rains during the harvest window may degrade grain quality. Consequently, an increased proportion of the Black Sea wheat crop may be categorised as feed quality.

London feed wheat futures started the week strongly, the November 2026 contract climbing to £180.05 at Monday’s close. After inching forward to £180.50 on Tuesday, the contract pulled back to £180.00 on Wednesday, before finishing Thursday at £180.50.

On Hectare Trading, feed wheat received bids up to £191 for May 2027 movement. Farmers across the country have been forward-selling feed wheat for movement from August this year though to the start of 2028.

For full spot and futures price analysis, visit our enhanced Insights on Hectare Trading.

Milling Wheat

One of France’s largest grain processors has forecast that the French soft wheat crop will be noticeably smaller this year (31.5–32.0 million tonnes) due to drought and heat in western regions. However, early harvest results indicate that the milling quality of the French crop is excellent, suggesting that UK growers will face robust competition from high-quality European milling wheat.

Meanwhile, heavy rainfall has affected the quality of China’s domestic wheat harvest, which could increase Asian import demand for milling wheat throughout the season.

Since closing at €209.50 (£180.52) on 24 June, the September 2026 Paris milling wheat contract gave up €8 to last week’s close at €201.50 (£172.73). A brighter start to this week saw the contract reach €204.75 (£174.88) on Tuesday, easing slightly on Wednesday then finishing Thursday at €205.00 (£174.77).

Feed Barley

The early winter barley harvest in Poland has disappointed farmers with average yields of 4.5–5.0 t/ha, while some drought-affected fields are producing only around 3 t/ha.

In the UK, the most immediate threat to feed barley prices comes from widespread quality issues in the malting barley sector caused by the European heatwave. High nitrogen levels and poor grain retention are causing a wave of rejections at the stores, so that a massive bottleneck of downgraded malting barley is being dumped into the feed market.

Farmers in the Midlands have received bids up to £176 for feed barley on Hectare Trading, for May 2027 movement, while we’ve also seen forward-selling to lock in prices in East Anglia and Northumberland & Scottish Borders.

Oilseeds

Canada shocked the market by estimating a record 23.4 million planted acres of canola for the 2026/27 season. However, severe weather events are already threatening this potential record crop, and there are now fears that up to 5% of the planted area could be abandoned.

Meanwhile, the spike in crude oil prices has caused another sharp rally in Paris rapeseed futures. The August 2026 contract climbed €8.75 to €512.75 (£438.60) on Monday, and then to €523.00 (£446.83) by Wednesday’s close. On Thursday, the contract eased back to €520.25 (£443.55).

On Hectare Trading, we’ve seen bids up to £439 in the Midlands for oilseed rape, to move this August.

Wanted Crop

🌾Feed wheat is wanted for collection in East Anglia, for movement next week. Guide price of £170–172/t ex-farm.

🌾 Group 1 and 2 wheat required for collection in East Anglia, the East Midlands and Yorkshire and the Humber, for July movement. Guide price of £188–192/t ex-farm.

🌾 Group 4 hard wheat is wanted for collection in Oxfordshire, Buckinghamshire and the West Midlands, for July movement. Guide price of £175/t ex-farm.

This article is for general information only and does not constitute advice. While we make every effort to ensure the accuracy of the content at the time of publication, Hectare Trading makes no guarantee regarding the data provided.