Wheat prices surge as export disruption rattles markets

Our benchmark spot prices (East Midlands)

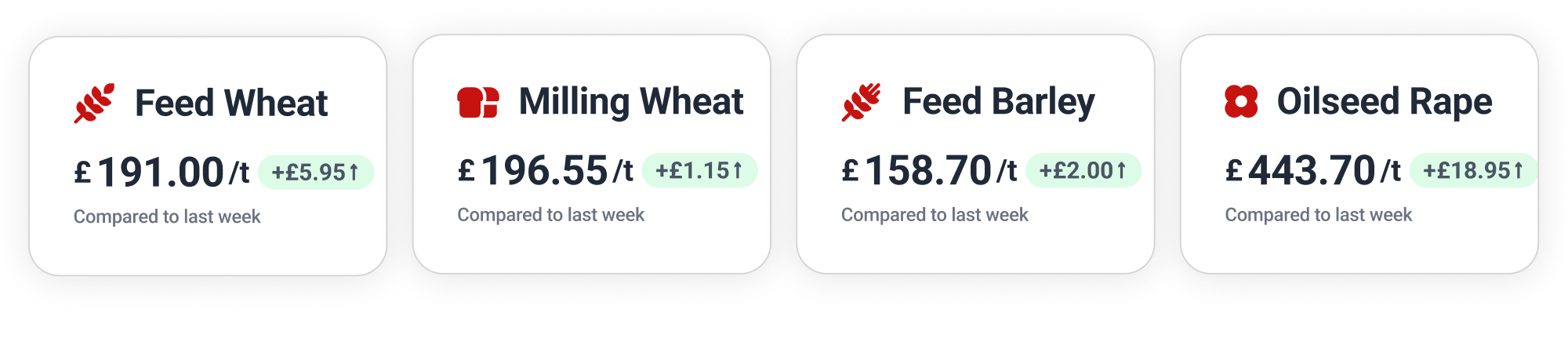

Feed Wheat

Grain markets have surged this week due to the potent convergence of Black Sea disruption, a surprisingly bullish USDA WASDE report, deteriorating European crop conditions and reignited Middle East tensions.

The rapid escalation of conflict in the Sea of Azov has choked off a route that typically handles approximately 25% of Russia’s wheat exports. Furthermore, a Russian strike on Kernel’s Chornomorsk terminal destroyed roughly 45,000 tonnes of wheat, reducing the port’s export capacity by a third just as harvest pressure builds.

After finishing last week strongly, London feed wheat futures have been on the charge this week. The November 2026 contract rose to £188.50 by Tuesday’s close, then shot up by £7 to £195.50 on Wednesday. Some easing back saw the contract end Thursday at £194.25.

In busy trading, feed wheat received bids on Hectare Trading up to £193 for September movement in the East Midlands – as domestic prices catch up with the rising futures. Across the country, farmers have been forward-selling feed wheat for movement from August this year through to May 2027.

For full spot and futures price analysis, visit our enhanced Insights on Hectare Trading.

Milling Wheat

The latest US WASDE report, released last Friday, delivered exceptionally lean supply projections, helping to boost prices for quality wheat.

US wheat production for 2026/27 is now estimated to be the lowest since 1970, at 41.8 million tonnes, down on last month’s projection of 42.0 million tonnes. This is largely due to reductions in hard red winter wheat (down to 471 million bushels from 804 in 25/26) and soft red winter wheat (down to 287 million bushels from 353 in 25/26).

Paris milling wheat has also enjoyed significant gains this week. From a close last Thursday at €205.00 (£174.99), the September 2026 contract climbed over €26 to finish Wednesday at €231.50 (£196.99). By Thursday’s close, the contract stood at €229.50 (£194.42).

Feed Barley

Extreme heat has decimated barley prospects across Europe, while at home there is major anxiety surrounding the UK spring barley crop, which has endured a very difficult growing season marked by a wet spring followed by an intense flash drought and heatwaves.

The UK winter barley harvest is progressing rapidly, but the results are highly variable. With malting crops failing to meet specification, an influx of downgraded malting barley has the potential to create a bottleneck in the feed market.

Oilseeds

EU rapeseed processing hit an all-time record of 26.3 million tonnes last season, driven almost entirely by demand from the biofuel sector.

In stark contrast to some Western European struggles, Ukraine is reporting an exceptional start to its rapeseed harvest. Early yields are averaging 1.94 t/ha, nearly 20% higher than at the same stage last year.

After starting the week with a jump to €527.75 (£450.33), August 2026 Paris rapeseed futures dipped to €522.50 (£445.25) on Tuesday. The contract rose again to €541.00 (£460.35) on Wednesday, before easing back to €535.75 (£454.87) by Thursday’s close.

Wanted Crop

🌾Feed wheat is wanted for collection in the East Midlands, for movement between October and December. Guide price of £182/t ex-farm.

🌾 Feed wheat required for collection in Northumberland & Scottish Borders, for July movement. Guide price of £180/t ex-farm.

🌾 Feed barley is wanted for collection in Yorkshire and the Humber. Movement this month, with a guide price of £155–160/t ex-farm.

This article is for general information only and does not constitute advice. While we make every effort to ensure the accuracy of the content at the time of publication, Hectare Trading makes no guarantee regarding the data provided.