Protein pressure ahead! Could 2026 be a tight year for group 1 wheat?

2-MINUTE READ

Rising fuel and fertiliser costs are already shaping decisions for the 2026 crop. With margins under pressure, many growers are reviewing nitrogen strategies – and that could have knock-on effects for group 1 wheat availability.

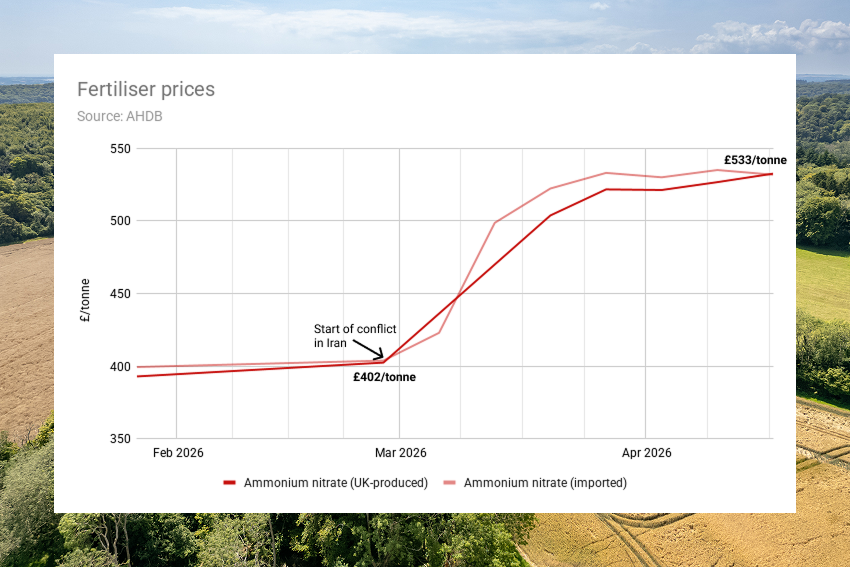

Since the conflict in Iran began on 28 February, the price of UK-produced ammonium nitrate fertiliser has risen from £402/tonne to £533/tonne, a 33% increase.

The cost of AN fertiliser has increased by 33% since the start of the conflict in Iran

Similarly, the price of UK red diesel jumped by 19.6% in one month, from 74.91 ppl in February to 89.61 ppl in March.

Impact of reduced applications

One obvious answer to rising input costs is to reduce fertiliser applications.

However, group 1 wheat varieties rely heavily on nitrogen to hit milling specification, particularly late-season applications. Even small adjustments can make a big difference.

AHDB guidance suggests that an extra 40kg N/ha applied late can add around 0.5% to grain protein, while an additional 80kg N/ha may add up to 1%. If fertiliser applications are trimmed, the risk of missing protein targets increases.

Supply can be highly sensitive: in the challenging 2024 season, only 31% of milling wheat samples met the 13% protein target. When crops fall short, wheat intended for milling often ends up in feed channels. At a national level, even a modest drop in protein achievement rates can tighten milling wheat supply and support premiums.

Opportunities for group 1 wheat

That’s a scenario buyers are already factoring into their thinking. If protein risks build through 2026, buyers may look to secure quality wheat earlier than usual.

We’ve already seen signs of this on Hectare Trading. Following the start of the conflict in Iran, bids on group 1 wheat for July 2026 or later movement strengthened noticeably, with several offers around £200/t appearing in late March.

Yesterday, the post-harvest November 2026 contract of London feed wheat closed at an eight-month high of £189.25, while September 2026 Paris milling wheat jumped over €5 to €214.25.

This raises the prospect of (at least partially) offsetting higher input costs by locking in higher prices post-harvest.

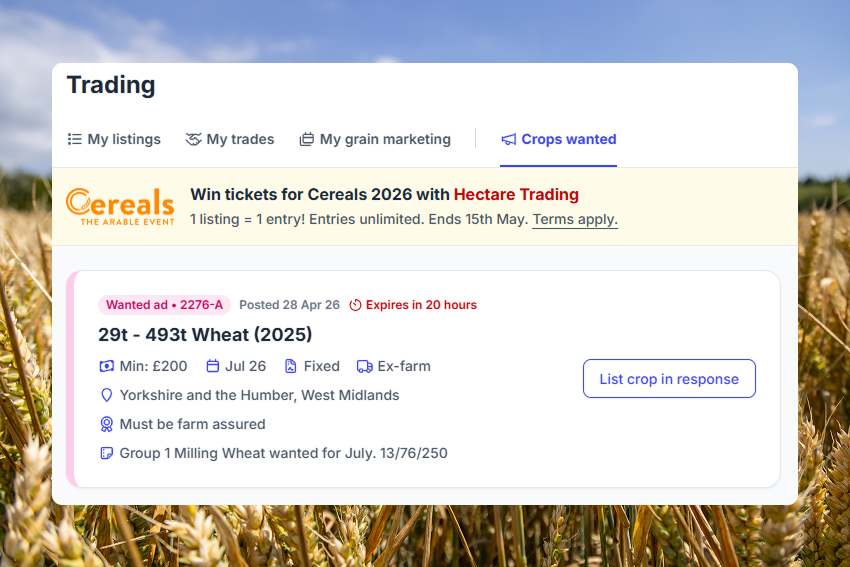

It’s also worth checking the Crops wanted section on Hectare Trading. This week, we’ve seen buyer demand for group 1 wheat for July 2026 movement at £200/t in Yorkshire and the West Midlands – an indication that forward demand is already present.

Keep an eye on “Crops wanted” to track buyer demand

For growers, rising input costs could create a strategic opportunity rather than just a challenge:

If you still have 2025 group 1 wheat to sell and can hold it until post-harvest, forward-selling now could allow you to take advantage of stronger buyer interest.

If you need to clear your shed, we’re currently seeing bids on 2025 group 1 wheat around £190/t for May movement (depending on location).

If you’re growing 2026 group 1 wheat, locking in a price on a portion of your crop early may help protect margins while uncertainty remains around fertiliser costs and protein outcomes.

Markets can change quickly, but tight protein supply – or even the expectation of it – often drives buyer behaviour ahead of harvest. Meanwhile, if buyers doubt UK supplies, they’ll source overseas – so it pays to act early when opportunities arise.

The simplest way to test current demand in your region is to list some grain now for post-harvest movement. That way you can test the market before making a commitment.

In uncertain times, keeping an eye on protein risk – and taking a proactive approach – forms a key part of your grain marketing strategy for quality wheat.

Got group 1 wheat to sell? Post a listing to see what buyers are currently prepared to pay in your region – with no obligation to sell.

This article is for general information only and does not constitute advice. While we make every effort to ensure the accuracy of the content at the time of publication, Hectare Trading makes no guarantee regarding the data provided.