Mixed signals on Iran war cause uncertainty in global grain markets

Our benchmark spot prices (Midlands & Wales)

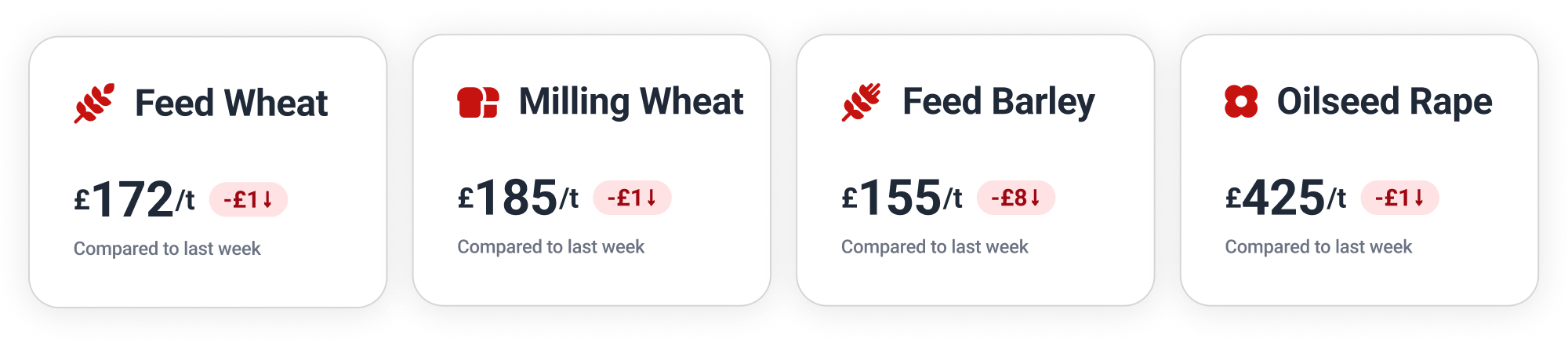

Feed Wheat

A succession of conflicting signals over the Iran war have caused uncertainty in global grain markets.

Meanwhile Egypt, competing with Indonesia as the world’s top wheat importer, is facing record-high domestic wheat prices due to a currency depreciation, soaring fuel costs and the Middle East conflict.

London feed wheat futures have lacked significant direction for much of this week. The “old crop” May 2026 contract climbed to £172.45 on Monday, before moving slightly lower to end Wednesday at £172.05. A marginal gain on Thursday saw the contract close at £173.40.

Farmers have been forward-selling 2026 feed wheat this week on Hectare Trading, locking in new crop prices in the East and West Midlands, Central Scotland and East Anglia.

For full spot and futures price analysis, visit our enhanced Insights on Hectare Trading.

Milling Wheat

Hot, dry and windy weather in the US have raised concerns over the condition of US hard red winter wheat. Upside price movement is, however, being capped by Russian exports, with March grain shipments estimated to reach 4.7 million tonnes.

Having dropped to €203.25 (£175.69) at the end of last week, Paris milling wheat (May 2026) started the week on the back foot, finishing Monday at €202.25 (£174.78). By Thursday’s close, the contract stood at €205.25 (£177.61).

On Hectare Trading, we’ve seen forward-selling of 2026 group 1 wheat for November movement in East Anglia. Farmers have also locked in new crop prices on group 4 soft wheat in Yorkshire and the Humber.

Feed Barley

The recent spell of dry and warm weather has improved ground conditions, helping to accelerate spring planting progress throughout the UK. Across the Channel, French spring barley planting is already 95% complete, well ahead of their five-year average.

Total barley production across the EU and the UK is forecast to fall to 59.3 million tonnes this year, down from 63.6 million tonnes in 2025.

Oilseeds

Strikes on critical energy infrastructure across Qatar, Saudi Arabia and the UAE helped send Brent crude oil briefly above $110 per barrel at the end of last week. The global oilseed complex has, however, stopped reacting heavily to every swing in the energy markets.

China slashed its imports of US soybeans by nearly 84% in January–February, heavily pivoting to Brazilian supplies. The USDA nevertheless expects a surge in China’s soybean imports to 108 million tonnes in 2026/27. Meanwhile, Ukrainian officials suggested the country may increase its rapeseed planting by a third (to 1.5 million hectares) if the conflict in the Middle East is prolonged.

Paris rapeseed (May 2026) has been hovering around the €500 mark this week, dropping to €497.50 (£429.94) on Monday, before recovering to €500.50 (£433.14) by Tuesday’s end. At Thursday’s close, the contract stood at €502.25 (£434.62).

Wanted Crop

🌾 Feed Barley is wanted for collection from across Central Scotland for movement between March and June with a guide price of £150–£156/t.

🌾 Milling Wheat (Group 1, 2 or 4 Hard) (10.2/74/130) required from across East Anglia, the East Midlands, Essex, Hertfordshire, Oxfordshire and Buckinghamshire. April movement with a guide price of £164–170/t for a home in Northamptonshire.

🌾 Milling Wheat (Group 3 or 4 Soft) (10.2/74/130) is wanted from across the East Midlands, Yorkshire and the Humber. April movement with a guide price of £170–173/t.

🫘 Feed Beans required for collection across the East and West Midlands, East Anglia, North, South and West Wales, Oxfordshire, Buckinghamshire, Essex and Hertfordshire. Wanted for movement between May and September, the buyer is happy to take 2025 or 2026 crop, with a guide price of £200–£215/t.

🌾 Oilseed Rape is wanted for collection across Essex, Hertfordshire, the North West, the South East, North Wales, the West Midlands, Oxfordshire, Buckinghamshire, Yorkshire and the Humber. April to July movement with a guide price of £430–£440/t (base excluding oil bonus).

🌾 Oilseed Rape required for collection across the East Midlands, for April movement with a guide price of £470–£480/t (fixed including oil bonus).

This article is for general information only and does not constitute advice. While we make every effort to ensure the accuracy of the content at the time of publication, Hectare Trading makes no guarantee regarding the data provided.