Wheat markets diverge as risk builds for 2026

3-MINUTE READ

Every day seems to bring another twist in the Middle East, with markets bouncing one way then another. For wheat growers, the fundamentals remain largely unchanged, but how long would the war in Iran need to drag on for this situation to change? And how should you approach marketing old and new crop when the outlook is so uncertain?

Wheat supply remains strong. According to the latest WASDE report, US wheat production for 2025/26 stands at 54.01 million tonnes – 6% higher than the 10-year average – while total US supply is unchanged from last month’s projection at 80.54 million tonnes.

The US is well supplied domestically but not dominant globally – with no change to projected exports.

Globally, projected wheat supply has edged slightly higher to 1,101.75 million tonnes. Ending stocks have dipped marginally to 277 million tonnes, but still sit at a five-year high.

For months now we have seen that old crop prices are being driven by supply – and that supply is comfortable.

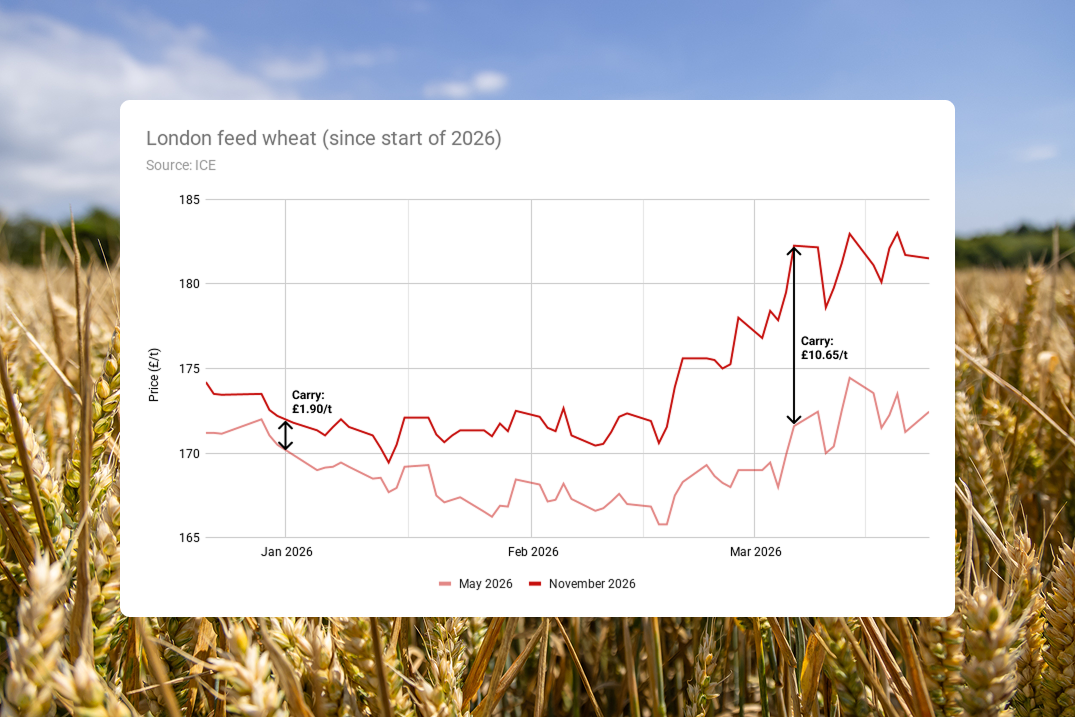

Old crop vs new crop: a widening gap

There are five London feed wheat futures contracts per year but the most heavily traded are May and November. These therefore act as the benchmarks for UK old and new crop pricing.

At the start of the year, the “old crop” (May 2026) price was just £1.90 below the “new crop” (November 2026) price. By 6 March, that gap had widened considerably to £10.65.

The carry between the May 2026 and November 2026 London feed wheat contracts has risen to £10.65

Rising energy and fertiliser costs due to the Iran war have increased production risk for 2026/27 crop. Weather uncertainty also poses a production risk supporting new crop prices.

In short, the old crop market is more supply-driven, the new crop market is more risk-driven.

You can lock in comparatively higher new crop prices now by forward-selling your 2026 wheat. This could be a good move if you’re uncertain how the geopolitical situation is going to develop.

If your budgets are constrained by the current financial year, it’s worth bearing in mind that the income from any harvest 2026 crop you sell now will only be realised when you move the crop in the next tax year.

War in Iran: delayed impact on supply

Unlike Ukraine, the Iran war is not directly removing wheat from the global market. Instead, it’s working indirectly with more delayed impact.

Around a third of global fertiliser trade passes through the Strait of Hormuz, now largely closed. The world’s largest urea plant, Qatar Energy, has also been shut down after attacks on its facilities.

The result has been a supply shortage, with US fertiliser prices rising by as much as 32%. Farmers have the choice of absorbing higher input costs or reducing fertiliser application.

The next fortnight is critical, as winter wheat in the US and Europe needs its final nitrogen application. If there is no clear resolution of the conflict – or at least a resumption of traffic through the Strait of Hormuz – the consequences are straightforward:

Reduced nitrogen application

Potentially lower yields in harvest 2026

A supply impact on 2026/27 wheat

Essentially, the longer the war continues, the higher the risk premium on new crop. Meanwhile, the abundant supply of 2025/26 grain reduces the impact on old crop prices.

Equally, a swift resolution in the Middle East could see new crop prices drop away suddenly. Without locking in harvest 2026 prices now, you could miss this opportunity while still having incurred higher diesel and fertiliser costs on your spring drilling and last winter wheat applications – the worst of both worlds.

Trading two markets at once

The Iran war focuses attention on the different price dynamics of old and new crop – which is why we’ve seen an increasing divergence of old and new crop prices.

For old crop, prices are shaped by the current availability of stocks, domestically and worldwide. Hence why the war in Ukraine – one of the world’s top 10 wheat producers – had such an immediate effect on prices.

For new crop, the market factors in the risk that the next harvest might disappoint – due to anything from poor weather to rising input costs. That creates opportunity, but also a high degree of uncertainty.

The key for UK growers is to recognise that you’re now operating in two different markets at once.

A balanced approach to grain marketing – taking advantage of stronger new crop prices while retaining some flexibility – may be the most sensible way to navigate what is likely to remain a volatile and fast-moving situation.

Want to lock in prices on your new crop? Or see what the local market has to offer for your old crop? Post a free listing today.

This article is for general information only and does not constitute advice. While we make every effort to ensure the accuracy of the content at the time of publication, Hectare Trading makes no guarantee regarding the data provided.