Global wheat glut deepens while US drought risks persist

Our benchmark spot prices (Midlands & Wales)

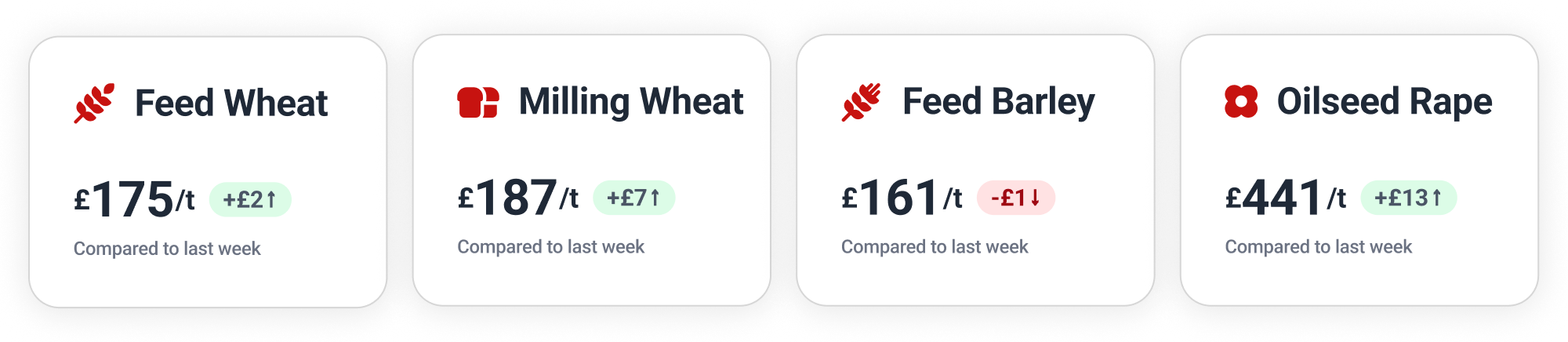

Feed Wheat

Last week’s US WASDE report indicated a worsening global abundance of wheat in 2025/26, an expansion of global wheat supply to 1,103.2 million tonnes combining with a contraction of global demand to 820.1 million tonnes. India in particular shows a reduction of projected demand by nearly 5 million tonnes between March and April.

This heavy supply picture is being compounded by Russia, as the government recently added 5 million tonnes to its export quota for wheat, meslin, barley and corn on the back of sufficient domestic supply.

The “old crop” May 2026 contract of London feed wheat started the week (May 2026) climbing nearly £3 to £175.95, after a disappointing end to last week. Modest gains continued, as the contract closed Thursday at £178.65.

Meanwhile, the gap between the May contract and the “new crop” November 2026 contract has shrunk, from over £11 at the end of March to just £3.75 on Wednesday.

For full spot and futures price analysis, visit our enhanced Insights on Hectare Trading.

Milling Wheat

Concern for this year’s US hard red winter wheat crop continues, due to drought across the Southern Plains. The USDA’s latest Crop Progress report revealed good-to-excellent ratings for winter wheat dropping to just 32% in Kansas, 15% in Texas, 14% in Nebraska and 10% in Oklahoma.

Meanwhile, Indonesia is now the world’s top wheat importer for the season at 13.2 million tonnes, due to rising demand from the country’s expanding flour milling industry.

Paris milling wheat prices have drifted following last week’s sharp decline, the May 2026 contract inching up to €195.75 (£170.42) on Monday before dropping away to €194.25 (£168.87) by Wednesday’s close. Thursday’s trading saw the contract settle at €194.00 (£168.86).

On Hectare Trading, some farmers have been locking in prices on their new crop. We’ve seen forward-selling of 2026 group 3 wheat for November movement in the West Midlands, 2026 group 4 hard wheat in the East Midlands and even some 2027 group 4 hard wheat in Northumberland & Scottish Borders.

Feed Barley

Australia shipped 1.5 million tonnes in February, with the feed component rising 11% over January to 1.13 million tonnes. China was the primary destination, absorbing over 900,000 tonnes of feed barley and 323,000 tonnes of malting barley.

Meanwhile, the UK malting barley market remains weak due to a lack of interest from brewers and maltsters, while in contrast the livestock sector is increasing demand for feed barley.

Oilseeds

Soybeans continue to drive prices in the global oilseed complex. Brazil raised its soybean harvest estimate to a record 179.2 million tonnes, which will likely lead to market saturation between May and July. However, China has announced a 3.1% drop in its soybean imports year-on-year from January to March, amid stricter quality inspections on Brazilian cargoes.

Canada’s rapeseed export programme is struggling, with cumulative shipments at 5.6 million tonnes compared to 7.2 million tonnes at the same point last year. Meanwhile, Ukraine is projecting a large expansion in rapeseed production for 2026/27, rising 25% to 4 million tonnes at the expense of soybeans.

After dipping back to €500.00 (£434.57) on Tuesday, Paris rapeseed (May 2026) surged over €9 to close Wednesday at €509.25 (£442.72). Another strong day saw the contract end Thursday at €516.75 (£449.78).

Wanted Crop

🌾 G1, G2 or G4 Hard Milling Wheat is wanted from East Anglia and East Midlands for April–May movement with a guide price of £170–177/t ex-farm.

🌾 G1 Milling Wheat is wanted from the West Midlands for April movement with a guide price of £183–185/t ex-farm.

🌾 Feed Barley is wanted from Northern England and Scotland for April–June movement with a guide price of £150/t ex-farm.

🌾 Feed Wheat is wanted from the West Midlands for April–May movement with a guide price of £177–182/t ex-farm.

🌾 Oats (min 44kg/hl) are wanted from the West Midlands and Wales (Mid, South, West) for April movement with a guide price of £120–128/t ex-farm.

This article is for general information only and does not constitute advice. While we make every effort to ensure the accuracy of the content at the time of publication, Hectare Trading makes no guarantee regarding the data provided.