Wheat prices surge as production forecasts collapse

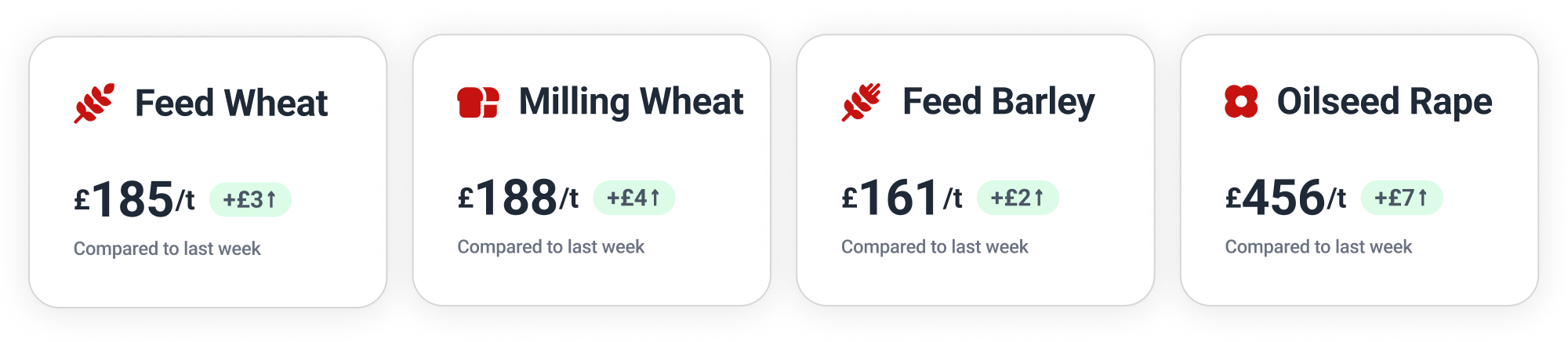

Our benchmark spot prices (Midlands & Wales)

Feed Wheat

While domestic feed wheat achieved its highest prices in over a year on Hectare Trading, the most significant market event of the week was the USDA’s latest WASDE report, which confirmed a massive supply contraction.

Global wheat production for 2026/27 was slashed by 24.8 million tonnes to 819.06 million tonnes. The US accounted for a major portion of this decline, with its wheat output cut to 42.49 million tonnes, the lowest since 1972.

Since sinking to a contract low of £165.80 on 17 February, London feed wheat (May 2026) has made consistent gains. Another jump early this week saw the “old crop” contract hit £195.00 on Tuesday – its highest level since June 2025 – before relaxing back to £187.70 at Thursday’s close.

Farmers have been taking advantage of the buoyant market on Hectare Trading, locking in prices on 2026 feed wheat in the East and West Midlands and North East Scotland

For full spot and futures price analysis, visit our enhanced Insights on Hectare Trading.

Milling Wheat

Persistently dry conditions in parts of the UK combined with high fertiliser prices have made farmers question the return on investment for late nitrogen applications aimed at boosting milling wheat protein levels. Some growers are concluding that the marginal cost of application outweighs the potential milling premium.

Globally, the biggest story remains the catastrophic failure of the US hard red winter wheat crop. The condition of US winter wheat has deteriorated further, with just 28% of the 2026 crop now rated at good or excellent.

Paris milling wheat futures have been choppy so far this month, the September 2026 contract rising over €10 from last Friday’s close at €206.25 (£178.22) to Tuesday’s €216.50 (£187.93). By Thursday’s end, the contract stood at €213.50 (£185.57).

On Hectare Trading, we’ve seen forward-selling of 2026 milling varieties in Central Scotland and the West Midlands.

Feed Barley

The dry weather is causing concern for UK spring barley establishment. As the domestic planted acreage is relatively small this year, there is very little flexibility to absorb a supply shock if production falls short.

Meanwhile, FranceAgriMer has raised its forecast for 2025/26 barley exports outside the EU to 3.8 million tonnes, the increase covered by an upward revision in supply figures.

Oilseeds

The FAO Vegetable Oil Price Index has reached its highest level since July 2022, strongly supported by biofuel demand and the rising cost of crude oil. Meanwhile, the USDA expects global soybean production to rise by 13.9 million tonnes next season. Currently, the market is heavily supplied by Brazil, which exported a record 16.8 million tonnes of soybeans in April, largely to China.

While Canadian canola planting is currently delayed across the prairies, export demand is surging. Following China’s decision to lower anti-dumping tariffs on Canadian canola seed and meal, exports hit a 17-month high of 1 million tonnes in March – 369,000 tonnes of which went to China.

Paris rapeseed (August 2026) climbed to €515.00 (£445.41) on Monday, and another €7 to €522.00 (£453.11) by Tuesday’s close. Some retracement over the next two days saw the contract finish Thursday at €517.00 (£449.38).

Wanted Crop

🌾 Feed wheat is wanted for collection in Yorkshire and the Humber for movement this month, with a guide price of £186–190/t ex-farm.

🌾 Feed wheat required for collection in the East Midlands. May movement with a guide price of £180–185/t ex-farm.

🌾 Feed wheat is wanted for collection in East Anglia. Movement in May or June, with a guide price of £175–180/t ex-farm.

🌾 Feed barley required for collection in Yorkshire and the Humber for movement this month, with a guide price of £166–170/t ex-farm.

🌾 Feed wheat is wanted for collection in Yorkshire and the Humber. Movement in May or June, with a guide price of £180–185/t ex-farm.

🌾 Feed wheat required for collection in Wales, the West Midlands and the North West. May or June movement, with a guide price of £185–193/t ex-farm.

This article is for general information only and does not constitute advice. While we make every effort to ensure the accuracy of the content at the time of publication, Hectare Trading makes no guarantee regarding the data provided.