Global wheat fortunes diverge amid weather extremes

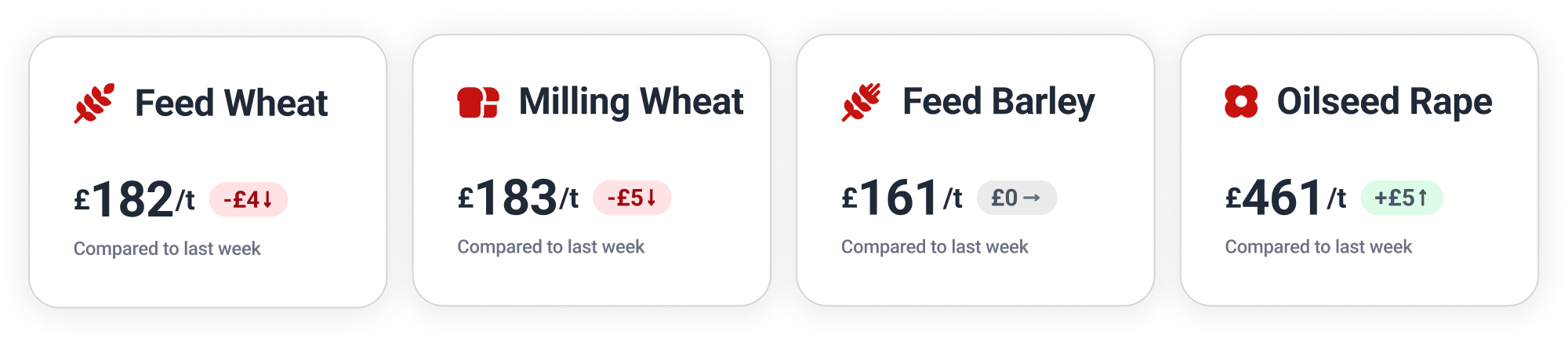

Our benchmark spot prices (Midlands & Wales)

Feed Wheat

Divergent weather patterns have led to contrasting fortunes for global wheat production.

With prolonged dry spells across Europe, the European Commission has reduced its EU wheat production forecast to 126.9 million tonnes, while the MARS crop monitor also trimmed average yield expectations.

Conversely, Turkey is projecting a relatively high wheat harvest of 23 million tons of wheat following favourable rainfall. In China, however, excessive rain has hampered crop development, with around 8 million tonnes of wheat now spoiled.

Following the long weekend, the November 2026 London feed wheat contract inched forward to £190.50 on Tuesday, before dropping back £2 to £188.50 by Wednesday’s close. With a lack of momentum the contract finished Thursday at £187.00.

Farmers have been forward-selling 2026 feed wheat on Hectare Trading this week, locking in prices in the South West, the East Midlands and Yorkshire and the Humber.

For full spot and futures price analysis, visit our enhanced Insights on Hectare Trading.

Milling Wheat

Asian buyers remain active in the milling wheat market, highlighted by the recent purchase of 100,000 tonnes from the US and Canada by a group of South Korean millers.

Meanwhile, the US winter wheat crop continues to decline to record lows, with just 26% now in good or excellent condition, against 50% a year ago. In Kansas, the leading producer of hard red winter wheat in the US, the figure is as low as 15%.

By contrast, 82% of the UK winter wheat crop has been rated in good or excellent condition, although the lack of rain is increasing concern.

From last week’s peak at €216.75 (£187.61), September 2026 Paris milling wheat fell over €4 to €212.50 (£184.42) on Monday, a further €2 to €210.50 (£182.68) by Wednesday, closing at €210.25 (£182.47) on Thursday.

Feed Barley

Global barley prices have increased by 9% year-on-year according to the IGC’s GOI index, driven by expectations that global barley consumption will continue to grow. Furthermore, Germany is actively targeting China as its next strategic market for opening up barley exports.

Ukrainian barley exports for the 2025/26 season have dropped by 55.5% compared to the same period last year, sitting at just 1.48 million tonnes. However, domestic barley reserves inside Ukraine have grown by 66.5% compared to last year.

Oilseeds

Oilseed markets have seen wild price fluctuations tracking the diplomatic negotiations between the US and Iran. Hopes of a ceasefire and the reopening of the Strait of Hormuz temporarily caused crude oil prices to drop by 6% on Monday, with a knock-on effect on the global oilseed complex.

Potentially boosting oilseed demand, Germany has agreed to raise its crop-based biofuels cap from 4.4% to 5.8%, to align with EU climate targets. However, industry groups are not expecting a large expansion in rapeseed acreage.

Paris rapeseed futures dipped markedly along with crude oil on Monday, the August 2026 contract dropping over €11 to €515.25 (£447.16). Prices quickly bounced back towards the recent two-year high, closing at €524.75 (£455.41) on Tuesday and €526.75 (£457.14) on Thursday.

In the West Midlands, farmers have been selling 2026 oilseed rape forward on Hectare Trading, locking in prices for August movement.

Wanted Crop

🫘 Feed beans wanted for collection in the South East, Essex and Hertfordshire. Guide price of £230 for movement in July.

🌾 Feed barley required for collection in the North West for June movement, with a guide price of £165–170/t ex-farm.

🥣 Milling oats wanted for collection in Mid Wales and the West Midlands. June or July movement, with a guide price of £115–135/t ex-farm.

🌾 Feed wheat required for collection in the East Midlands for July movement, with a guide price of £195/t ex-farm.

🌾 Feed wheat is wanted for collection in East Anglia, the East Midlands and the South East. 2026 crop for movement in September, with a guide price of £187/t ex-farm.

🌾 Feed barley required for collection in the West Midlands, the South, Oxfordshire and Buckinghamshire. Movement this month, with a guide price of £160/t ex-farm.

🌽 Grain maize (feed) required for collection in East Anglia, the East Midlands, the South East and Yorkshire and the Humber. Movement between August and December, with a guide price of £210/t ex-farm.

🌾 Group 1 or 2 wheat (11.5/200/74) wanted for collection in the East Midlands. June or July movement, with a guide price of £195/t ex-farm.

This article is for general information only and does not constitute advice. While we make every effort to ensure the accuracy of the content at the time of publication, Hectare Trading makes no guarantee regarding the data provided.