US–Iran deal eases input fears but pressures oilseeds

Our benchmark spot prices (Midlands & Wales)

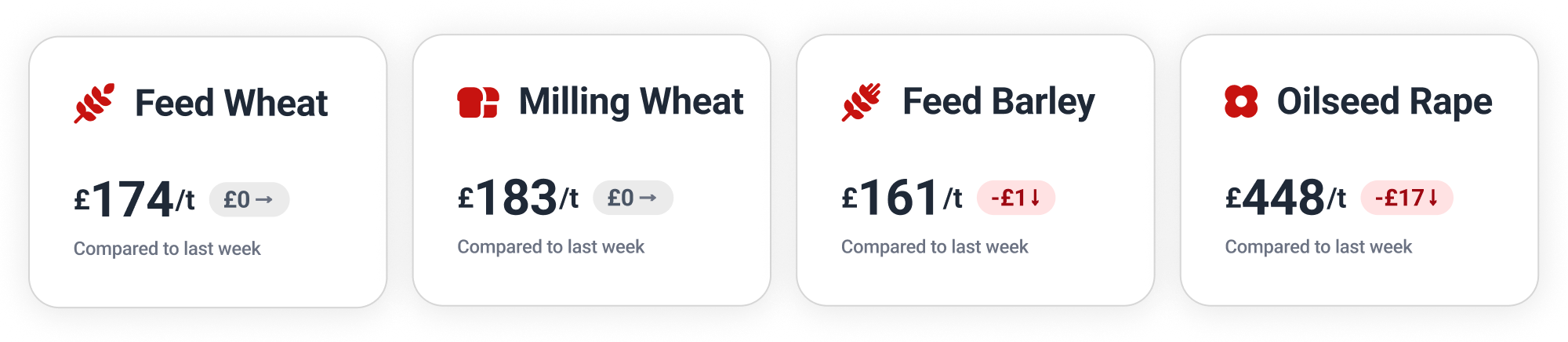

Feed Wheat

The dominant macroeconomic driver this week was the US–Iran framework agreement to reopen the Strait of Hormuz, easing immediate fears over agricultural input costs ahead of the 2027 planting season.

Global wheat supplies remain comfortable due to massive upgrades in the Black Sea region. The latest WASDE raised Russian wheat production projections for 2026/27 to 88 million tonnes, while Ukrainian output was raised to 23.5 million tonnes, due to favourable spring weather conditions.

The November 2026 London feed wheat contract dropped over £2 on Monday to a three-month low of £177.25. The rest of the week saw a patient recovery, the contract rising to £179.75 on Wednesday, before closing Thursday at £179.00.

On Hectare Trading, feed wheat in the Midlands has received bids up to £187 for July movement. Meanwhile, farmers have been locking in prices on 2026 feed wheat, selling forward in North East Scotland and the East Midlands.

For full spot and futures price analysis, visit our enhanced Insights on Hectare Trading.

Milling Wheat

Persistent heavy rains in the US soft red winter wheat belt are delaying harvest and raising severe crop quality concerns. This is on top of the WASDE’s downgrade to the US wheat harvest, cutting production to 42.01 million tonnes, due largely to the poor US hard red winter crop.

At home, given high fertiliser costs and the inherent weather risks involved in achieving the required protein and quality specifications, many growers are questioning whether milling wheat carries too much financial risk – raising concerns over future domestic supply.

September 2026 Paris milling wheat started the week drifting below €200, closing Monday at €199.75 (£172.75). Successive days of gains brought the contract back to €203.50 (£175.95) on Wednesday, before easing to €203.25 (£175.89) at Thursday’s close.

We’ve seen bids on Hectare Trading this week for group 1 wheat up to £204 in the Midlands, for July movement, with farmers also selling 2026 group 1 wheat forward in the South West, for September movement.

Feed Barley

Recent rainfall has significantly aided grain fill for UK barley, though there are mixed expectations for the harvest. While spring barley crops suffered from moisture stress earlier in the season due to prolonged dry and warm conditions, recent rains have provided welcome relief.

On Hectare Trading this week, feed barley achieved bids up to £155 in the Midlands, moving in June or July.

Oilseeds

The US–Iran deal placed downward pressure on the global oilseed complex throughout the week, although doubts over the durability of the ceasefire remain.

Brazil has confirmed a bumper soybean harvest of 180.3 million tonnes, 5.1% higher than the previous record set last year. This means that Brazil’s soybean production has now grown by 56.7% since 2017, dramatically impacting the global market.

Following significant weather delays, Canadian farmers have rapidly accelerated their canola planting, reaching 73% of the intended acreage by early June. While Canada’s raw canola exports dipped in April due to weaker demand from Japan, the US is aggressively boosting its purchases of Canadian canola oil, due to strong biofuel demand.

Paris rapeseed futures have been fragile throughout the week, the August 2026 contract dropping €9 to €513.25 (£443.87) on Monday, then closing Tuesday at €507.50 (£438.84). After a brief respite on Wednesday, the contract fell away again to €502.00 (£435.65) by Thursday’s close.

Wanted Crop

🌾 Feed barley is wanted for collection in Yorkshire and the Humber for July movement, with a guide price of £160/t ex-farm.

🌾 Group 4 (hard) wheat required for collection in the East Midlands and Yorkshire and the Humber. July movement, with a guide price of £180/t ex-farm.

🌾 Feed wheat is wanted for collection in Yorkshire and the Humber. Movement this month, with a guide price of £186–190/t ex-farm.

🌾 Group 4 (soft) wheat required for collection in East Anglia, the East Midlands, Essex, Hertfordshire, Oxfordshire and Buckinghamshire. June or July movement, with a guide price of £193–196/t ex-farm.

This article is for general information only and does not constitute advice. While we make every effort to ensure the accuracy of the content at the time of publication, Hectare Trading makes no guarantee regarding the data provided.