Fertiliser prices drop as Hormuz traffic resumes

Our benchmark spot prices (East Midlands)

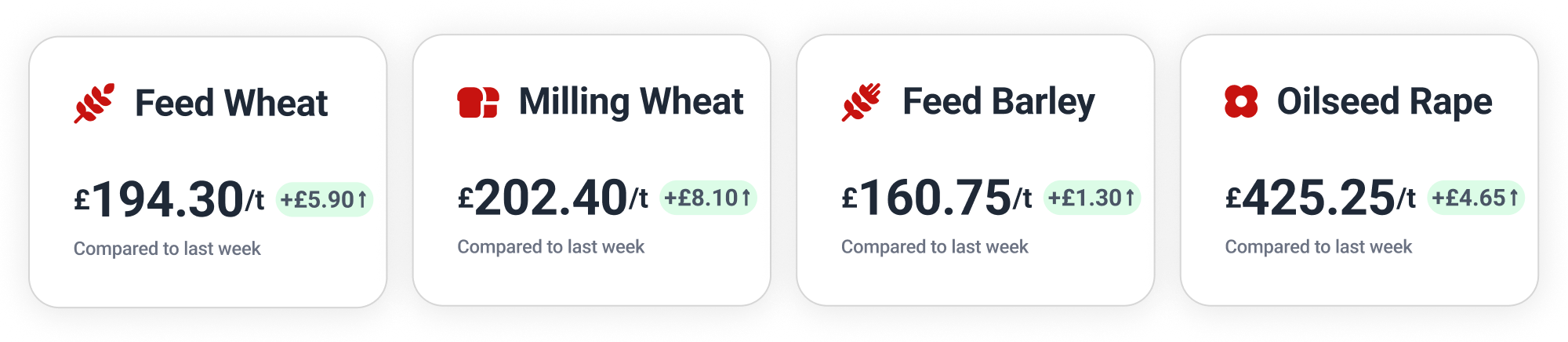

Feed Wheat

The resumption of shipments through the Strait of Hormuz has caused a sharp correction in fertiliser prices, with urea prices in the Middle East down roughly 50% to $475 per tonne.

As harvest is now underway in the Black Sea region, the upside for feed wheat is capped globally by strong production prospects in Russia and Ukraine. Meanwhile at home, the present heatwave is unlikely to have a major impact on UK winter wheat, with the crop so close to maturity.

Since falling to £177.25 on 15 June, the November 2026 London feed wheat contract has made slight but steady gains, reaching £180.85 at Monday’s close, and £181.50 on Wednesday. The contract pulled back to £179.25 by Thursday’s end.

On Hectare Trading, feed wheat in the Midlands received bids up to £186 this week for July movement, and up to £189 for movement next May. Farmers across Scotland, Wales and North East England have been locking in prices on 2026 and 2027 feed wheat.

For full spot and futures price analysis, visit our enhanced Insights on Hectare Trading.

Milling Wheat

Morocco, traditionally a major buyer of European wheat, has slapped a 135% tariff on imports for June and July, expecting a bumper domestic harvest of 9 million tonnes following years of drought. However, Moroccan flour millers are reporting severe quality issues with the domestic crop, meaning the country will still need to turn to the international market for quality wheat.

September 2026 Paris milling wheat climbed €6 on Monday to €207.25 (£179.20). After retreating slightly on Tuesday, the contract closed Wednesday at €209.50 (£180.52), before finishing Thursday back at €206.00 (£177.46).

Farmers have been forward-selling 2026 milling wheat on Hectare Trading this week, locking in prices in Oxfordshire & Buckinghamshire, the South, Essex & Hertfordshire, the East and West Midlands and East Anglia.

Feed Barley

The June MARS Bulletin has projected an average yield of 5.09 t/ha for winter and spring barley in the EU, with Romania and Bulgaria in particular performing well. This is a 10% drop on last year but 2% higher than the five-year average.

The European malting barley market is heavily oversupplied. With a distinct lack of demand from maltsters and brewers, much of this excess is expected to be diverted into the feed market, dragging down prices.

On Hectare Trading, 2026 feed barley has achieved bids up to £179 in the Midlands this week for movement next May, while we’ve also seen forward-selling in East Anglia and Central Scotland.

Oilseeds

In Brazil, soybean plantings are expected to hit a new record of over 49 million hectares, while in the US soybean acreage estimates have increased. The US and Brazil are fiercely competing for market share in China, the world’s largest soybean buyer. Brazil currently supplies over 60% of China’s imports.

By contrast, the global rapeseed market is finding support due to mounting weather-related supply risks in France, Germany, Australia and China.

Paris rapeseed futures recovered early this week, the August 2026 contract rising to €511.75 (£442.50) on Monday, then €518.00 (£446.52) by Tuesday’s close. After slipping back slightly on Wednesday, the contract regained ground to €518.75 (£446.88) at Thursday’s end.

Farmers have been selling 2026 OSR forward on Hectare Trading this week for August movement, in Essex & Hertfordshire and Northumberland & Scottish Borders. We’ve also seen 2027 OSR selling in North East Scotland.

Wanted Crop

🌻 Oilseed rape is wanted for collection next month across Scotland and Northumberland, with a guide price of £440/t ex-farm (base excluding bonus), depending on location.

🌾 Feed wheat required for collection in the North West, North Wales or West Midlands to take direct to a farm in Cheshire. July movement, with a guide price of £185–192/t ex-farm.

🌾 Group 1 wheat (13/76/250) is wanted for collection in the South West and West Midlands, for July movement. Guide price of £190/t ex-farm.

🌾 Feed barley required for collection in Yorkshire and the Humber for July movement, with a guide price of £155–164/t ex-farm.

This article is for general information only and does not constitute advice. While we make every effort to ensure the accuracy of the content at the time of publication, Hectare Trading makes no guarantee regarding the data provided.