USDA acreage surprise fails to lift wheat market

Our benchmark spot prices (East Midlands)

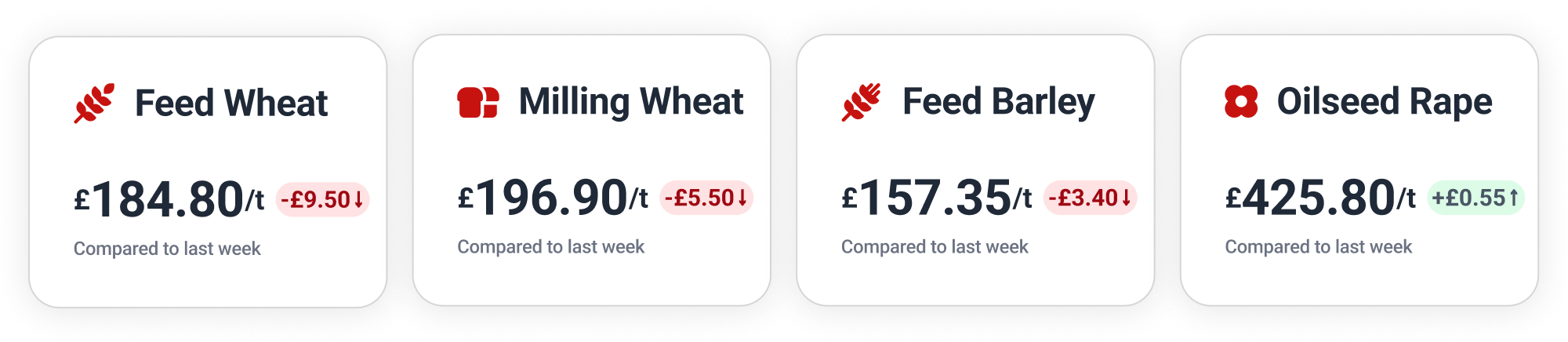

Feed Wheat

The global wheat market experienced a jolt following Tuesday’s highly anticipated USDA Acreage and Grain Stocks reports.

A record low US wheat planted area of 42.7 million acres, down 6% from last year, fell well below expectations, but global prices remain pressured by large carryover stocks – US wheat stocks rose 8% year-on-year to 920 million bushels – and accelerating harvest pressure from the Black Sea region.

After hitting £181.50 last Wednesday, the November 2026 London feed wheat contract declined by over £4 to £177.25 by this Monday’s close. A brief recovery on Wednesday brought the contract back to £179.50, before ending Thursday at £178.50.

On Hectare Trading, we’ve seen a range of bids for feed wheat in the Midlands up to £188, for movement this month.

For full spot and futures price analysis, visit our enhanced Insights on Hectare Trading.

Milling Wheat

The French durum wheat harvest is proceeding ahead of schedule, with 19% complete against 4% at the same point last year. However, only 58% of the crop is in good or excellent condition, as against 64% a week earlier and 71% a year ago.

Meanwhile, Algeria’s state grain buyer recently purchased 800,000 to 900,000 tonnes of milling wheat for delivery in August, supporting European prices, while South Korean millers bought 100,000 tons of milling wheat from the US.

Paris milling wheat futures have followed a similar pattern to London, the September 2026 contract dropping to €202.50 (£174.59) on Monday, and another 50 cents on Tuesday, before recovering very slightly to €203.00 (£174.53) by Wednesday’s close. A lack of momentum saw the contract close Thursday at €202.00 (£173.05).

On Hectare Trading this week, 2025 group 1 wheat received bids up to £196 in the Midlands, for July movement.

Feed Barley

The UK winter barley harvest has begun exceptionally early in parts of Suffolk, Norfolk and Cambridgeshire, with early reports indicating functional but not exceptional yields.

Meanwhile in France, the winter barley harvest is progressing rapidly at 42% complete, compared to a five-year average of 14% for this point of the year. Grain quality is generally good, with 71% rated good or excellent.

Oilseeds

The USDA raised its estimate for US soybean plantings to 85.4 million acres, while US soybean stocks rose 5.3% to 28.9 million tonnes. Meanwhile, Canada forecast a record increase in canola plantings to 23.4 million acres, reflecting a significant shift away from wheat.

Brazilian soybean exports remain robust, shipping over 14 million tonnes in June, with China still the main destination. The price gap between US and Brazilian soybeans is narrowing as US prices weaken.

Since peaking at €513.25 (£439.90) last Thursday, August 2026 Paris rapeseed drifted down to €505.25 (£433.05) by Tuesday’s close. The contract picked up to €508.75 (£436.05) on Wednesday, then closed Thursday back at €504.50 (£432.40).

Wanted Crop

🌾 Group 1 wheat is wanted for collection in the West Midlands and Yorkshire and the Humber, for July movement. Guide price of £190–195/t ex-farm.

🌾 Hard milling wheat (10.2/74/130) required for collection in the East Midlands. July movement, with a guide price of £185–188/t ex-farm.

🌾 Feed wheat is wanted for collection in Northumberland & Scottish Borders, the West Midlands and Yorkshire and the Humber, for July or August movement. Guide price of £177–182/t ex-farm.

🌾 Group 3 wheat required for collection in East Anglia, the East Midlands, Essex, Hertfordshire, Oxfordshire, Buckinghamshire, the South and the South East. July movement, with a guide price of £185–195/t ex-farm.

This article is for general information only and does not constitute advice. While we make every effort to ensure the accuracy of the content at the time of publication, Hectare Trading makes no guarantee regarding the data provided.